Everywhere you turn, you read about housing shifting back toward a buyer’s market. From Insider’s “3 signs the housing market is slowing down,” to US News and World Report’s, “Is Housing the Next Shoe to Drop for the Economy? Homebuilder Confidence Plunges in July,” you’re left to believe that the record-setting growth in home prices we’ve seen over the last few years is coming to an end.

On the other hand, Zillow’s zip code market report emails paint a completely different picture of housing confidence.

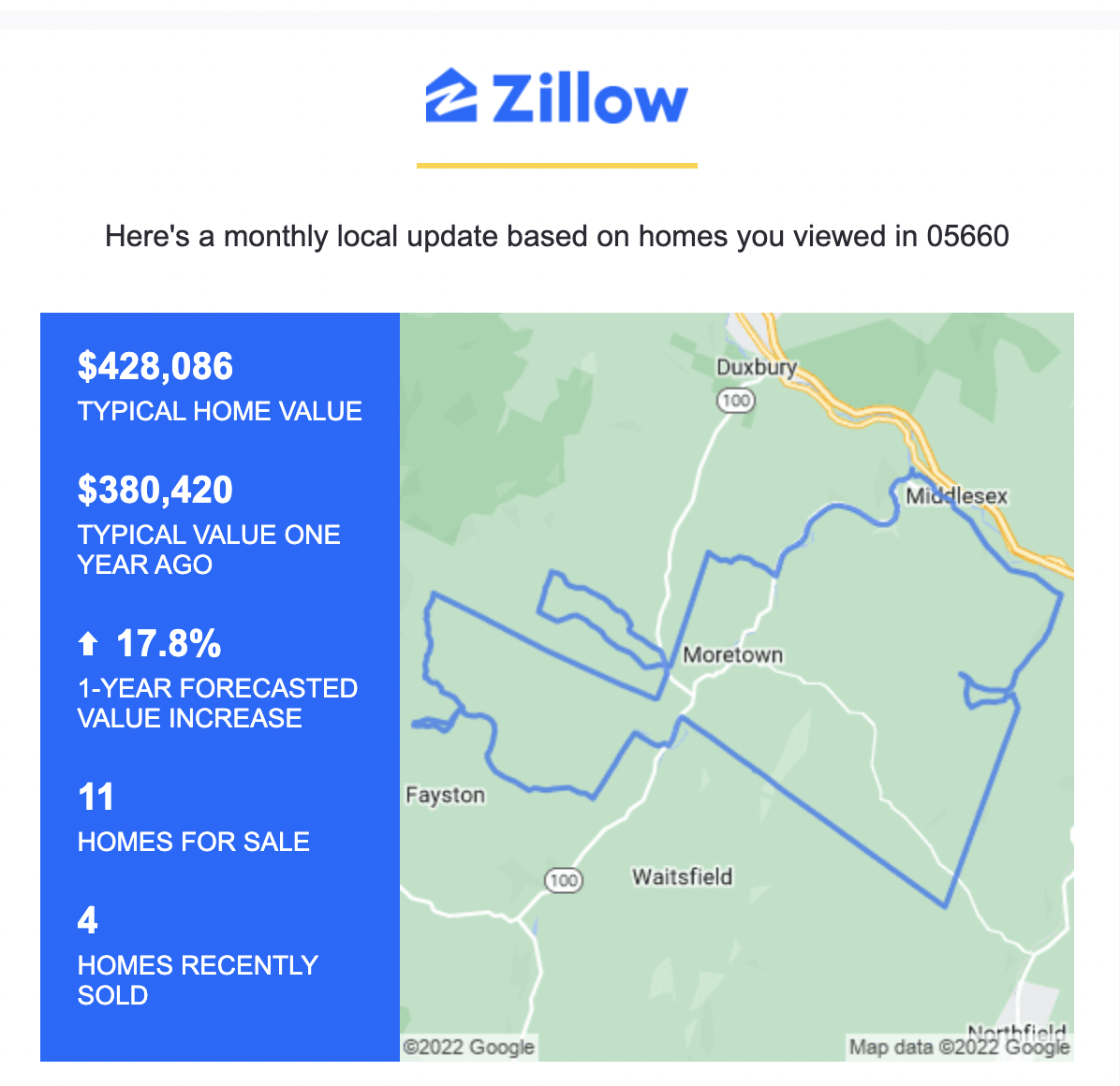

I get monthly emails from Zillow that predict average value appreciation for the zip code of my country home in Vermont. Each month for the past year or so, Zillow has predicted an annual appreciation in the high teens. Recently, they claimed that this time next year my home could be worth 17.8% more by the summer of 2023!

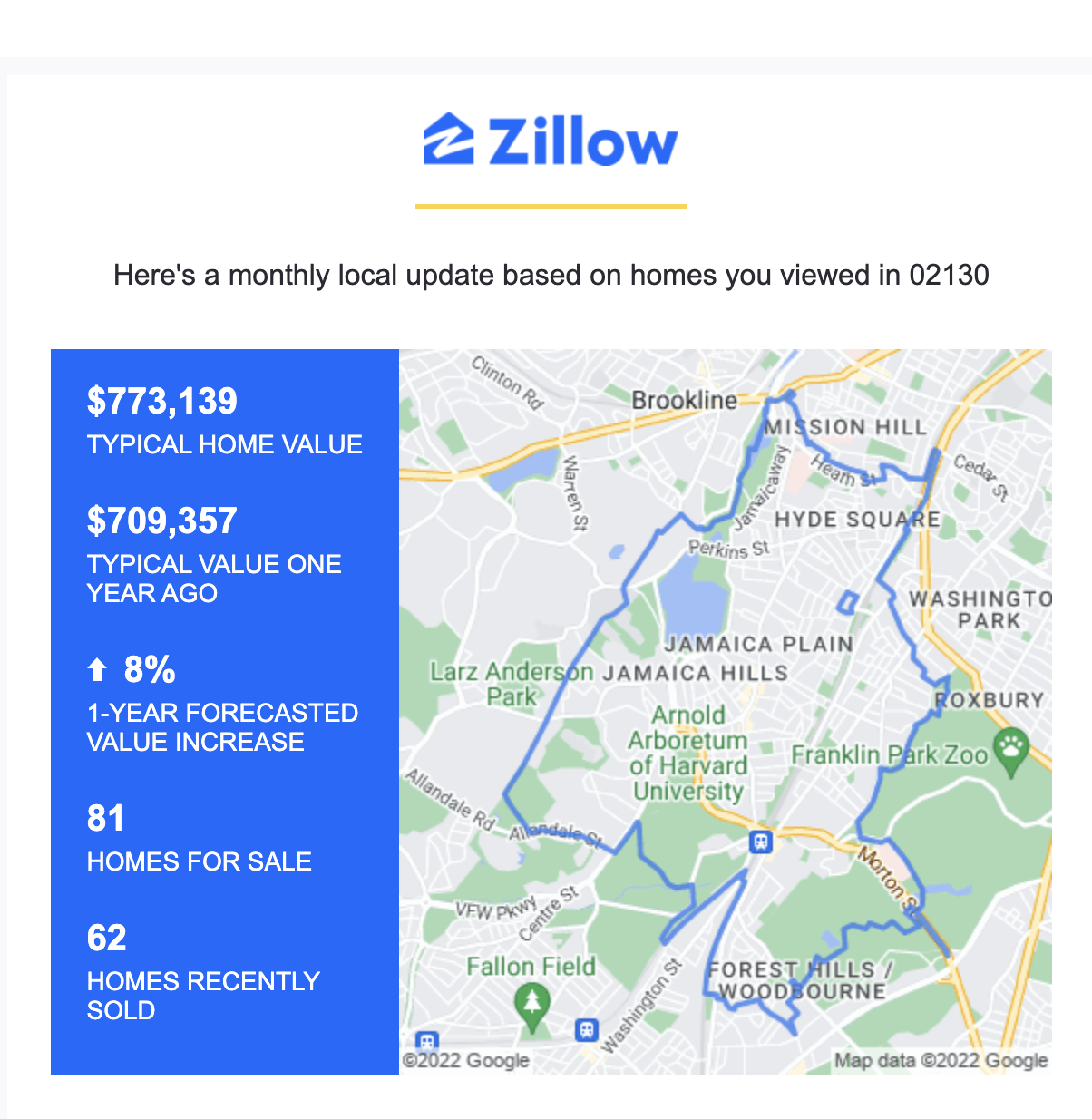

Thinking this country-area zip code could be an anomaly, I looked at a zip code for a property in Boston’s neighborhood Jamaica Plain, where Zillow predicted an 8% one-year forecasted growth.

While these kinds of appreciation rates would be great for homeowners’ equity, it’s hard to believe that appreciation will continue at this record-setting pace.

Sure, there’s still a lot of demand for homes in the U.S.. However, the borrowing costs those buyers have to shoulder has gone up considerably over the last year. In fact, the monthly cost of the average mortgage in the U.S. has gone up 40% since the start of the year. So, while many people still want to buy a home, the price of the home they can afford has gone down.

Interest rates and inflation

Interest rates have been going up because the Federal Reserve has been raising rates to slow inflation. With the most recent inflation report in July showing inflation remains stubbornly high, the Fed has committed to big additional interest rate increases. For prospective homebuyers, this means mortgage interest rates continue to rise in the second half of 2022– further increasing borrowing costs and lowering the price lots of folks can pay for a home.

With all this in mind, the question remains: Why is Zillow predicting such strong continued growth in the housing market?

First, there’s a chance that Zillow’s Market Reports are determined primarily by historical buying patterns in the area, and ignores central banking activity at the Fed that impacts affordability and, by proxy, home price growth.

The housing market is a little more complicated than simple supply and demand. Yes, those factors are very important, but another factor looms large — the cost of borrowing capital, or the interest rate on your mortgage.

Second, projecting a sinking market might not be in Zillow’s best interests. Zillow makes money by selling leads to Realtors. If Zillow’s marketing to homeowners makes them believe now is still a good time for them to sell, that might give more homeowners confidence to sell with a Zillow agent.

Also, Zillow would want to signal to prospective homebuyers that prices are continuing to go up, and the time to buy is now. At the end of the day, the more homes that trade and the more buyers and sellers using their platform, the more revenue they’ll see.

Third, Zillow could be factoring in all relevant indicators on future growth, and know something that many leading economists and real estate experts don’t! For instance, despite rising interest rates, Zillow’s data might signal that institutional investors with significant cash-on-hand could step in and continue to drive up housing prices across markets. Or, they could simply predict that housing demand will continue to outstrip supply but such a vast magin that the only place for housing prices to go is up.

Regardless of how or why Zillow is still predicting this appreciation, I, personally, remain skeptical. Surveys of home builders are showing wavering confidence and even some prices dropping. Lenders are rewriting mortgage pre-approvals, as they need to do every 90 days, and the rates are only climbing.

I think there’s more evidence for price growth flattening than continued appreciation. So, while I have absolutely no intention of selling, I also don’t think my home will be worth 17.8% more in 12 months. I’ll let you know how it turns out!

David Friedman is CEO and co-founder of Knox Financial.

This column does not necessarily reflect the opinion of RealTrend’s editorial department and its owners.

To contact the author of this story:

David Friedman at [email protected]

To contact the editor responsible for this story:

Tracey Velt at [email protected]