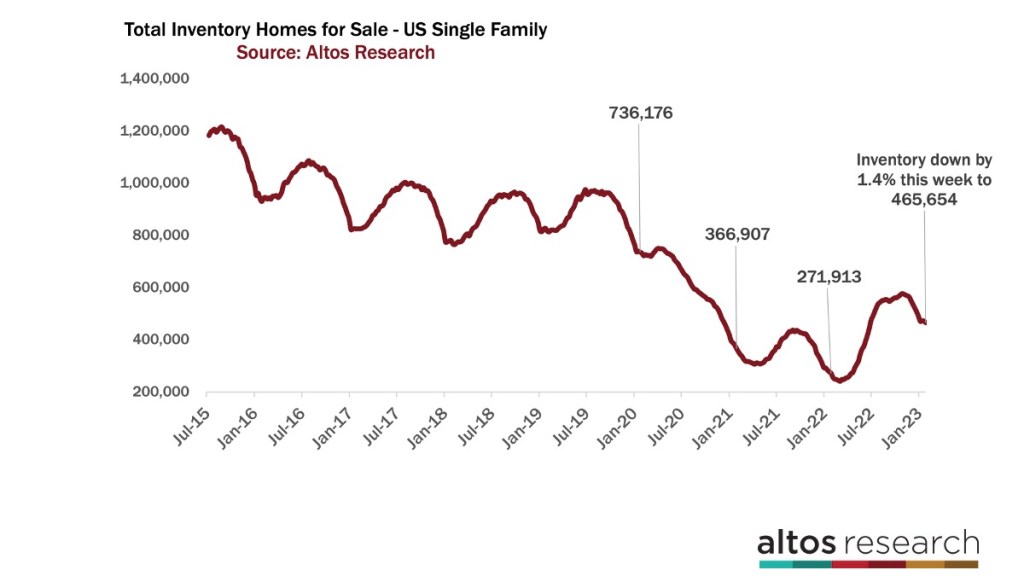

The available inventory of homes for sale continues to fall at the end of January. This data is created by a combination of a lack of new listings and an increase in buyer demand. The low level of supply is helping to stabilize prices which were falling in the 4th quarter.

So the question is: have we already seen the bottom for the housing market? Or, is this a temporary blip, a red herring, before an inevitable recession hits or interest rates climb again?

Everyone has their view of course, but here’s the data as we know it, right now. One thing to keep in mind about measuring housing activity in the U.S. is that so much action happens in the first and second quarters. If you were one of the folks who had a bearish view of the housing market in 2023, the early data is working against you.

The state of housing inventory

Available inventory of single family homes declined again this week to 466,000. That is surprising, though not entirely unheard of in late January. In pre-pandemic years it was normal for inventory to bounce up and down in each week of January and settle at the absolute low point for the year during the first week of February. It would then turn higher for the spring buying season.

I’ve been anticipating that this year’s data would return to more normal, pre-pandemic patterns, so we would expect the inventory low to hit next week and then climb reliably starting in February. Except that this year the inventory hasn’t been bouncing. Instead, the inventory has been falling each week.

We had a small increase in inventory a couple of weeks ago. Now, there are fewer homes on the market than at any time since the end of June last year. In that sense, the data shows an inventory curve for the spring of 2023 that is starting to look more like the markets of the last two years. There are very few sellers but there are plenty of buyers to gobble up what little inventory is available.

Inventory is 71% higher now than it was at the peak of 2022. In 2022, inventory continued to fall until the week of March 5. Inventory is still 37% lower than it was in January 2020, just before the COVID-19 pandemic. In summary: inventory is low, and it hasn’t begun the typical Spring climbing, so there should be at least one more week of decline.

But if this year starts to resemble the years of the COVID-19 pandemic, 2020, 2021 and 2022, then inventory could keep falling through all of February. That would be a surprise.

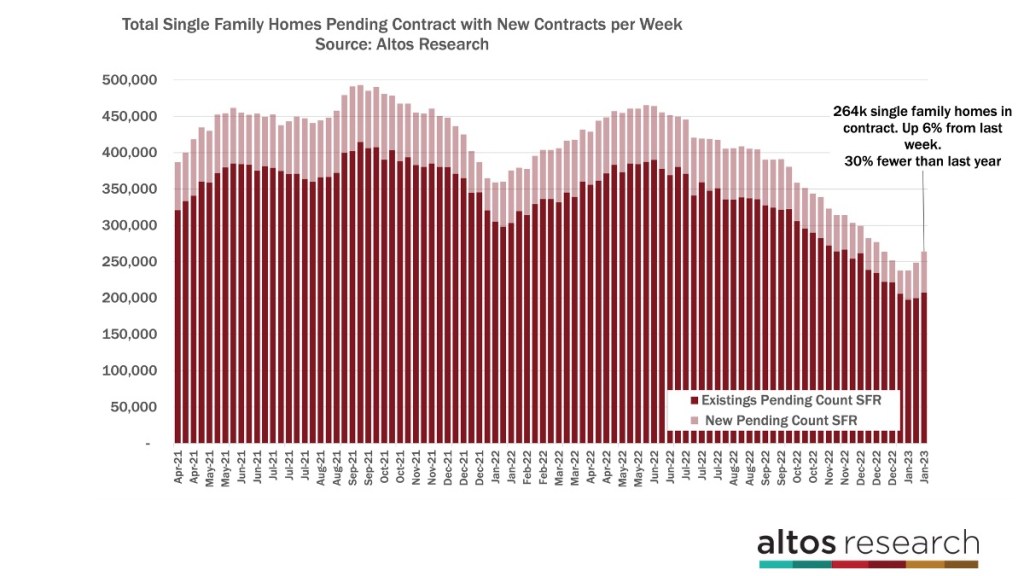

Pending home sales increase

We can see demand improving as pending sales are up 6% week over week. Pending sales are those homes in that are under contract but that do not have a closed sale yet. There are 30% fewer contracts pending now than there were last year, but that gap is closing as demand picks up from the ice-cold 4th quarter.

A few weeks ago, there were 35% fewer pendings compared to a year prior. These improving statistics are evidence that people are buying homes this spring. New pendings are up 16% week over week.

We have only 21% fewer homes going into contract this week. The sales gap between this year and 2022 is narrowing. Last year, the sales rate was elevated because everyone was rushing to take advantage of the last of the 3% mortgage rates.

In this chart each bar is the total count of homes in contract each week. The light portion of the bar are those newly in contract, otherwise known as the sales rate.

Sales rates are still much slower than last year when rates were still at 3.5% and buyers knew it was their last opportunity. But rather than trending downwards, they’re picking up each week.

Again, if you’re a buyer on the sidelines hoping for carnage in the housing market so you can swoop in for a great deal — there just isn’t any sign of that in the data.

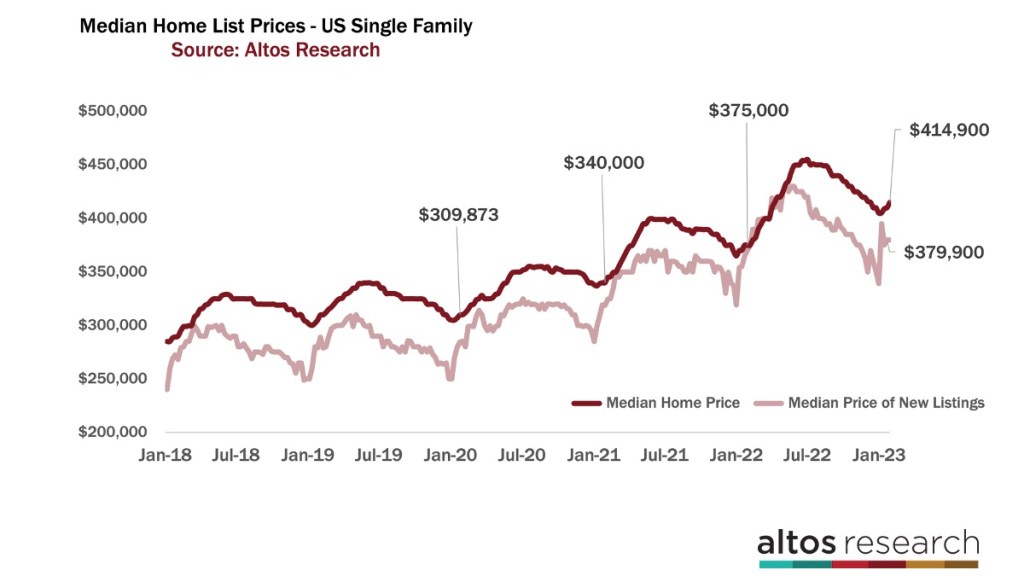

Climbing home prices

In response to the surprising amount of home buyer interest, and the tight supply of available inventory, home prices climbed by 1.2% this week to just under $415,000. It’s not a ton of price strength. It’s not skyrocketing. It’s not like last year. But, home prices aren’t falling like we were anticipating as recently as December.

When we talk about home prices holding up, it’s probably best to think about it as “sustaining” rather than home prices rising or falling. The median price of the newly listed homes this week, the light red line on the chart, is unchanged from last week at $379,900 and that’s only slightly above last year at this time.

The median price of those 264,000 homes under contract is the same as it was last year. So, while we see price stability, the year-over-year comparison is compressing so the annual percentage change in home prices is flat, or down, for 2023.

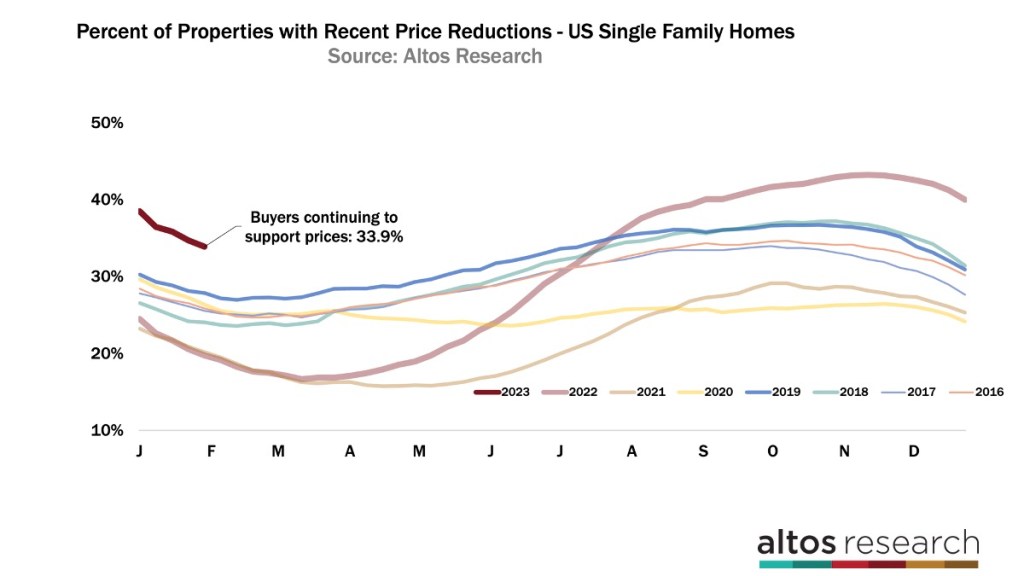

Dwindling price reductions

We see evidence of the demand in the price reduction data too. Because there are buyers out there, and because supply is so limited, the number of homes with price cuts keeps falling. Only 33.9% of the active market has taken a price cut recently. In this chart, each line is a year. You can see 2023 starting at the left end of the chart on a pretty steep down curve.

The trajectory looks more like the COVID-19 pandemic years than pre-pandemic years. Previously, 2019 had the most price reductions because 2018 was a year of rising mortgage rates. 2019 is the blue line here.

You can see we’re aiming down there now. I don’t think price cuts will drop under 30%, but home buyers don’t have easy pickings in this market. The best properties have multiple offers. Anecdotally, those offers — I hear — are coming in around the asking price. These are not bidding wars over asking.

Price increases

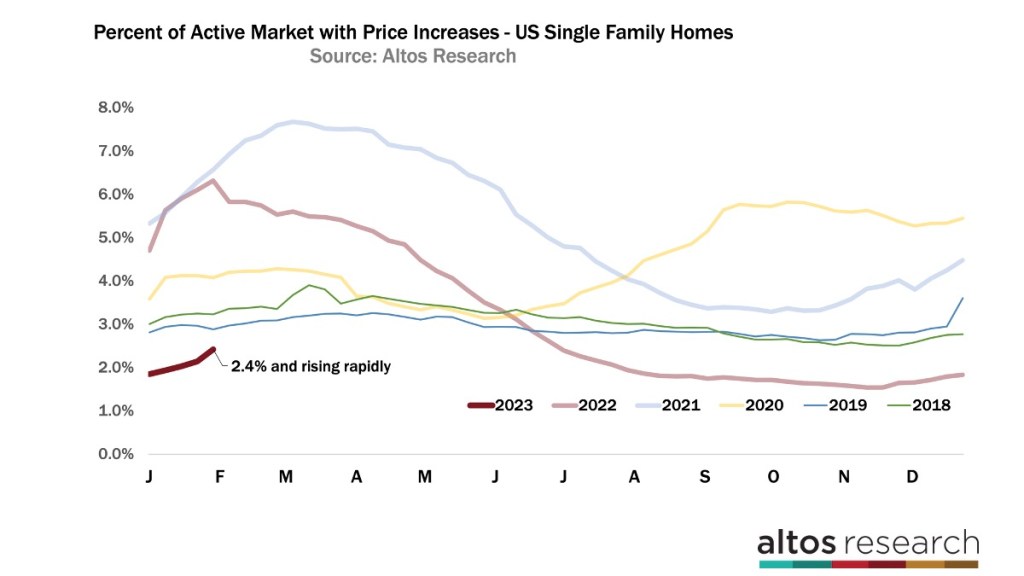

This is a statistic that I don’t often dive into. However, the number of price increases is moving now and that sheds more light on the market. These are homes that are on the market now that were previously on the market at a lower price. Very often these are fix-and-flips, investor activity, iBuyers, that kind of thing. Each line here is a year. When this number is higher, we have higher investor activity, stronger demand. Investors are very sensitive sellers. When this number falls it’s because investors see less demand.

You can’t keep increasing the price in the face of falling demand. Normally about 3% of the market has had a price increase. During the frenzy periods you see these huge spikes. Anywhere from 6% to 8% of the market is being flipped by investors during the spikes. In February 2022, the light red line had an abrupt turn. Investors pulled back. Investor buying stopped cold. You could argue that this statistic — percent of homes on the market with price increases — was the first signal the moment the market turned last year. Now, we see price increases rising rapidly from their very low levels of the fall.

The dark red line indicates 2.4% of the market has had a price increase. That’s rising substantially each week now. Keep your eyes on this pricing statistic to understand the sustainability of this spring market.

Your home buyers and sellers have a very different idea of the housing market this spring than what is actually happening. Do your potential sellers realize that the buyers are already looking? They need you to be the expert for them.

Mike Simonsen is president of Altos Research.